How to Accept Crypto Payments as a Business in 2026

The Practical Listing

The global stablecoin cross-border payments market is now valued at US$17.9 trillion, with B2B activity dominating at US$14.7 trillion, according to FXC Intelligence. The world’s crypto-holding population sits at over 560 million people, per Triple-A’s 2024 ownership data. Accepting crypto, in 2026, is no longer a marketing flourish; it’s payment infrastructure that competitors are already running.

This listing walks through what it actually takes to accept crypto payments as a business: the workflow, the seven best gateways on the market, the integration paths, and the compliance picture you’ll deal with on day one.

What does it mean to accept crypto payments?

To accept crypto payments means letting customers pay for goods or services with digital assets such as Bitcoin, Ethereum, or stablecoins (USDT, USDC), then receiving the value as crypto, as fiat to your bank account, or held in a stablecoin treasury wallet. A crypto payment gateway sits between the customer’s wallet and your books: it generates the invoice, verifies the on-chain transaction, locks the rate, and routes the settlement.

Two custody models exist. Custodial gateways hold the funds briefly before settlement and usually offer fiat conversion. Non-custodial gateways push value directly from the customer’s wallet to yours; you keep the keys, and the gateway only handles the rails. Both are mainstream in 2026; the choice depends on whether you want simpler accounting or maximum sovereignty.

Why businesses accept crypto payments in 2026

Three drivers explain the shift. The first is settlement speed: blockchain confirmations clear in seconds, while a traditional cross-border bank wire still consumes 5 to 7 working days for international processing. Fees come second; stablecoin payment rails routinely run between 0.4% and 1.5% per transaction, against the 1.5% to 3.5% (plus flat per-transaction fees) typical of card processing. The third reason matters most for risk-heavy verticals: blockchain finality, which makes the chargeback essentially obsolete.

“Stablecoin gateways are no longer just experimental tools. They are becoming core infrastructure for global payments.” — FXC Intelligence, 2026 Buyer’s Guide

A few categories pull harder than the rest. iGaming, Forex, SaaS sold to international audiences, e-commerce stores serving 50+ countries, payroll for distributed teams, creator-economy payouts: all of them carry a structural reason to want a crypto payment gateway. The reason is rarely ideological. It’s operational.

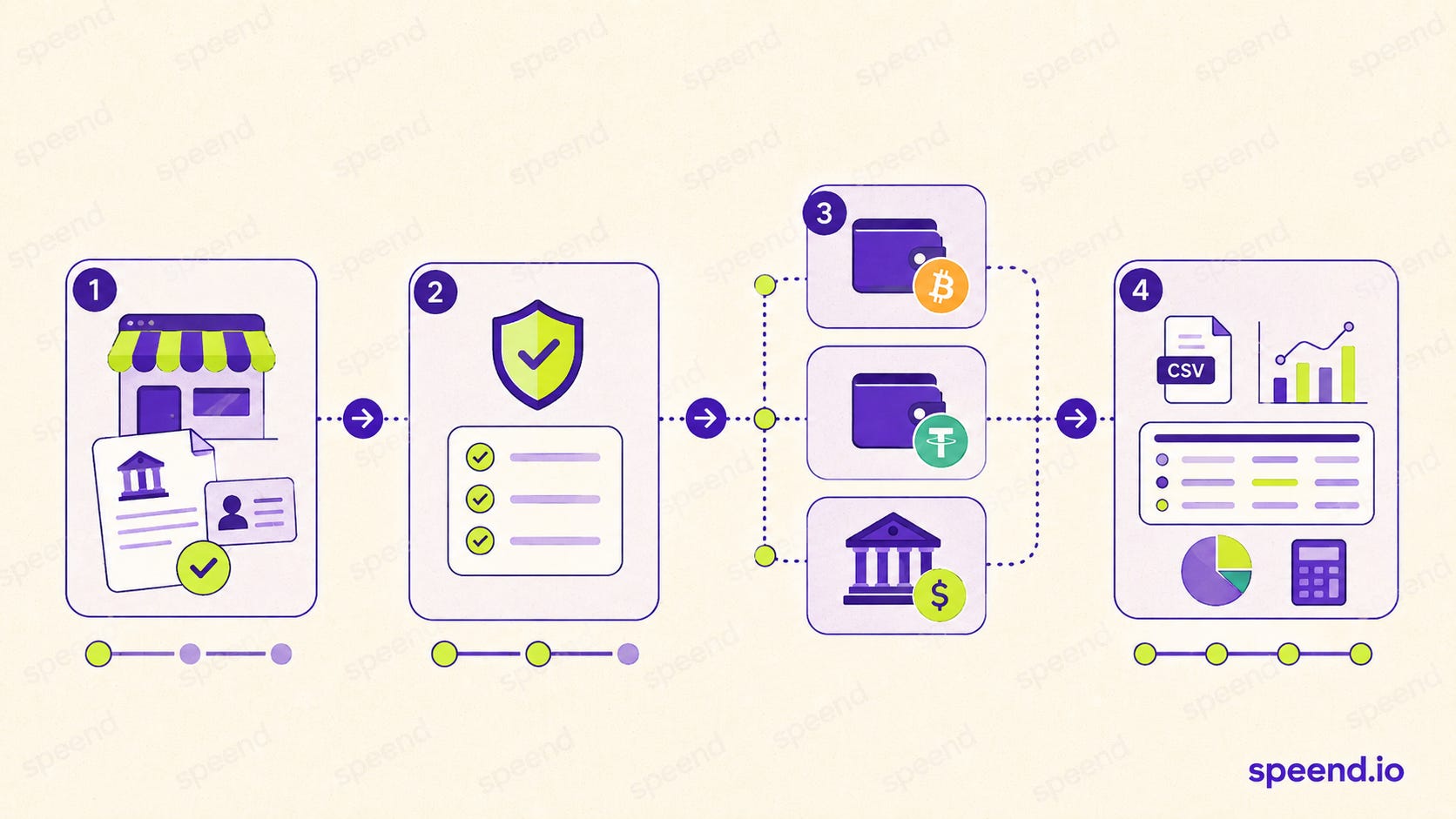

How to accept crypto payments as a business: the practical workflow

Below is the sequence almost every merchant runs through when adding a crypto payment gateway, regardless of provider.

Define the acceptance model. Decide whether settlement will be in crypto, in stablecoins, in fiat, or a configurable mix. This single choice cascades into licensing, custody architecture, accounting workflow, and tax reporting.

Pick a gateway. Evaluate coverage (which coins and chains), fees, settlement currencies, KYB requirements, and the developer experience. The “best” gateway depends entirely on what you sell and where your buyers are.

Pass KYB. Most reputable processors require business verification before activating live payments. Speed varies wildly: some onboarding flows clear in hours, others stretch to a week.

Integrate. Use a plugin (Shopify, WooCommerce, Magento, PrestaShop, OpenCart, WHMCS), a hosted checkout link, or a REST API with webhooks. Test in sandbox before going live.

Configure conversion rules. Auto-convert to a stablecoin if you want to neutralize volatility; auto-convert to fiat if you need predictable cash flow; hold the original asset if you’re treasury-positive on crypto.

Ship the checkout. Add the crypto option to your payment selector. Keep the messaging plain (”Pay with crypto”) rather than jargon-heavy.

Monitor, reconcile, report. Pull CSV exports for accounting, reconcile on-chain hashes against invoices, and report to tax authorities according to local rules.

A note on step 4: the integration time crypto vendor pages typically quote (2 to 4 weeks) is for full custom builds. Plugin installs take an afternoon. The reason businesses still budget weeks is reconciliation and finance review, not code.

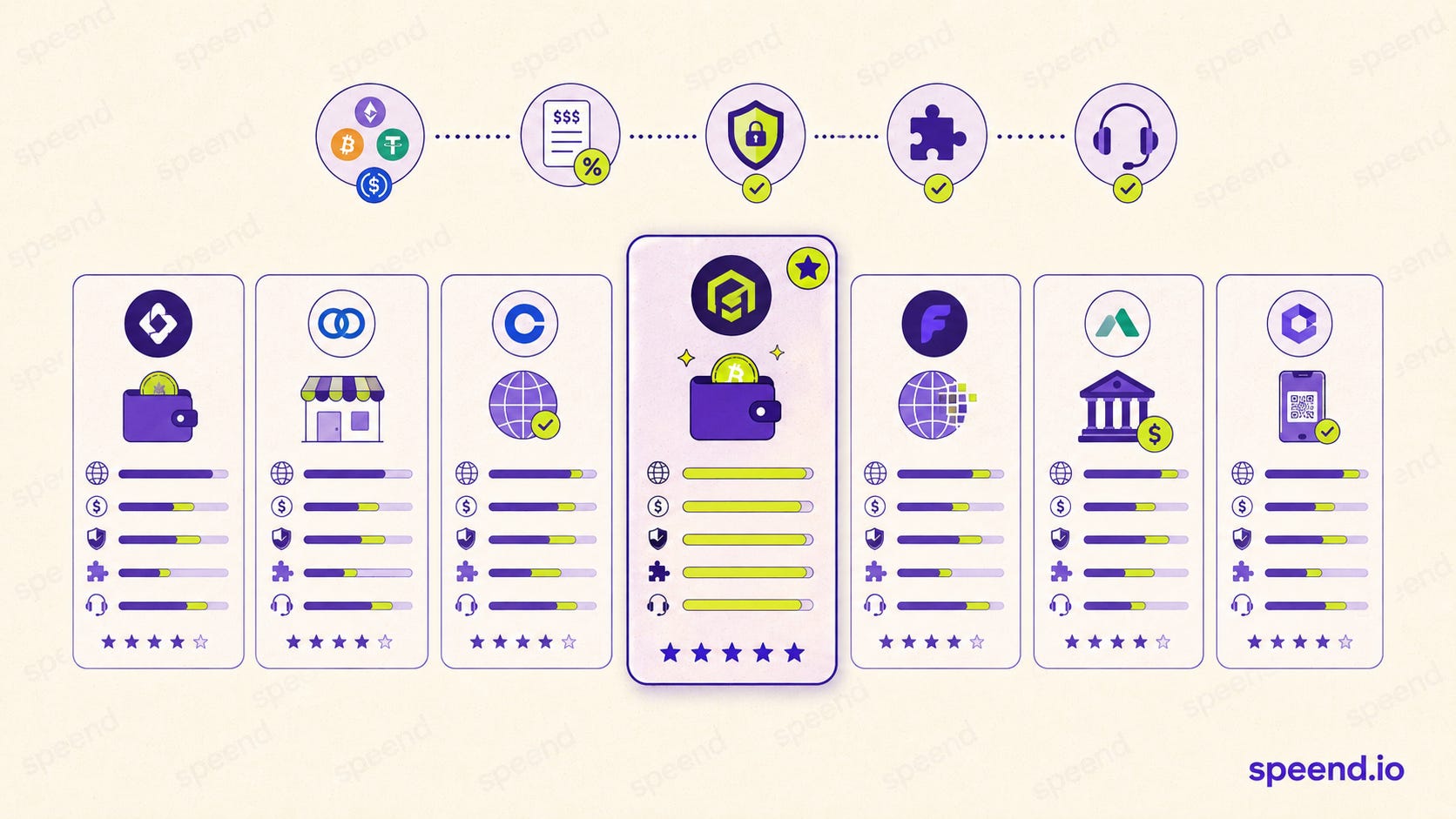

Top crypto payment gateways to accept crypto payments for business (2026 listing)

The list below is ordered by overall fit for typical merchants in 2026. It’s deliberately compact: ten options become noise. Seven is the working set most procurement teams actually shortlist.

1. Speend

Speend is a crypto payment gateway and crypto processing platform engineered for businesses that want to go live fast and stay live without operational drag. The platform supports 300+ coins across the major networks (Bitcoin, Ethereum, Tron, BNB Chain, Solana, Polygon, and more), runs a hassle-free KYC/KYB onboarding flow, and pairs every merchant with a personal manager backed by 24/7 support.

What sets Speend apart for working merchants:

Coverage: 300+ coins out of the box. Customers pick the asset they actually hold; you settle on your terms.

Onboarding: minutes to first invoice. KYC/KYB doesn’t drag the launch sideways.

Friendly REST API: documented endpoints, predictable webhooks, full sandbox environment. Engineering teams typically ship the integration in a single sprint.

Mass payouts and crypto payrolls: bulk-send to thousands of wallets in a single batch, ideal for distributed teams, affiliate networks, contractor payouts, and creator platforms.

Personal manager + 24/7 support: a real human who answers during incidents, not a ticket queue.

Low fees: pricing scaled to volume, with rates that stay competitive as you grow.

If you sell internationally, run an iGaming or Forex platform, operate a SaaS with global users, or pay distributed teams, Speend is where most procurement processes will end. Start at speend.io.

2. NOWPayments

NOWPayments covers the broadest coin universe of any major processor: more than 300 cryptocurrencies, with non-custodial settlement and fees starting at 0.5%. Plugins exist for WooCommerce, Shopify, Magento, PrestaShop, and WHMCS. Direct fiat settlement runs through third-party partners; for native bank settlement, you’ll route through an off-ramp.

Best for: stores with altcoin-heavy buyer bases, fast deployments, and merchants who want a non-custodial flow.

3. CoinGate

CoinGate holds an EU MiCA license and supports 70+ cryptocurrencies. It settles directly to EUR, GBP, or USD, includes Bitcoin Lightning Network for fast on-chain payments, and offers crypto refunds, which is genuinely rare in this category. Standard pricing sits around 1% per transaction with no setup fee.

Best for: European merchants needing clear MiCA alignment, and any business prioritizing compliance reporting and refund support.

4. BitPay

Founded in 2011 and now serving the likes of Microsoft and AMC, BitPay operates as the long-running enterprise-grade gateway. It settles daily to bank fiat across USD, EUR, GBP and others; supports 100+ assets accounting for over 90% of global crypto market cap; and runs strict KYC. Higher fees, in exchange for the most mature compliance posture in the category.

Best for: large enterprises that want bank-level settlement, predictable accounting, and the regulatory weight of a long-tenured processor.

5. Coinbase Commerce

Coinbase Commerce is the natural pick for merchants already inside the Coinbase ecosystem. Flat 1% fee on all transactions, automatic conversion to USDC, plus integrations with WooCommerce, Primer, and JumpSeller. The asset list is shorter than NOWPayments by an order of magnitude.

Best for: small-to-mid stores that want a recognizable brand on the checkout and a clean stablecoin settlement path.

6. CryptoProcessing by CoinsPaid

CryptoProcessing, the merchant product from CoinsPaid, handles 20+ major cryptocurrencies and converts to 40+ fiat currencies, with transaction fees under 1.5%. Licensed in Estonia, audited independently, with particular strength in iGaming and Forex.

Best for: high-volume merchants in transaction-intensive industries; teams that want a back office tailored to accounting workflows.

7. BTCPay Server

BTCPay Server runs as the open-source, self-hosted, Bitcoin-only processor. No fees beyond the network itself, full Lightning Network support, total custody control. The trade-off is real: you operate the infrastructure.

Best for: technically capable, Bitcoin-aligned merchants who refuse custodial models on principle.

How to choose a crypto payment gateway: the working checklist

Selection is rarely about the longest feature list; it’s about the shortest list of dealbreakers. Run candidates through these checks in order:

Settlement currency. Will you receive crypto, stablecoins, fiat, or a configurable mix? If you need bank-rail fiat, half the market drops out immediately.

Coin and chain coverage. Cover what your customers actually pay in. USDT-TRC20 dominates emerging markets; USDC-ERC20 dominates US merchants; BTC remains the universal floor.

Total cost, not just headline fee. Compare the headline percentage to the network fees, the conversion spread, the withdrawal fee, and any FX margin. The published rate is usually not the all-in rate.

KYB friction. Some processors clear in an hour; others take a week of compliance back-and-forth. Match this to your launch timeline.

Developer experience. API doc quality, webhook reliability, sandbox availability, SDK breadth. A developer can usually tell within 30 minutes whether the integration will be painful.

Plugin coverage for your stack (Shopify, WooCommerce, Magento, etc.) if you don’t want a custom build.

Support model. Personal manager versus ticket queue. The difference is invisible until something breaks at 2 a.m. on a Sunday.

Compliance posture. Licensed in your operating market. Especially relevant in the EU (MiCA), the UK (FCA registration), and the US (state-by-state Money Transmitter Licenses plus federal AML rules under FinCEN).

A practical heuristic: if your business is in steady growth and you want a single provider you won’t have to migrate from at $50K/month volume, Speend handles the same shape of operation at $5K and at $5M without a rebuild.

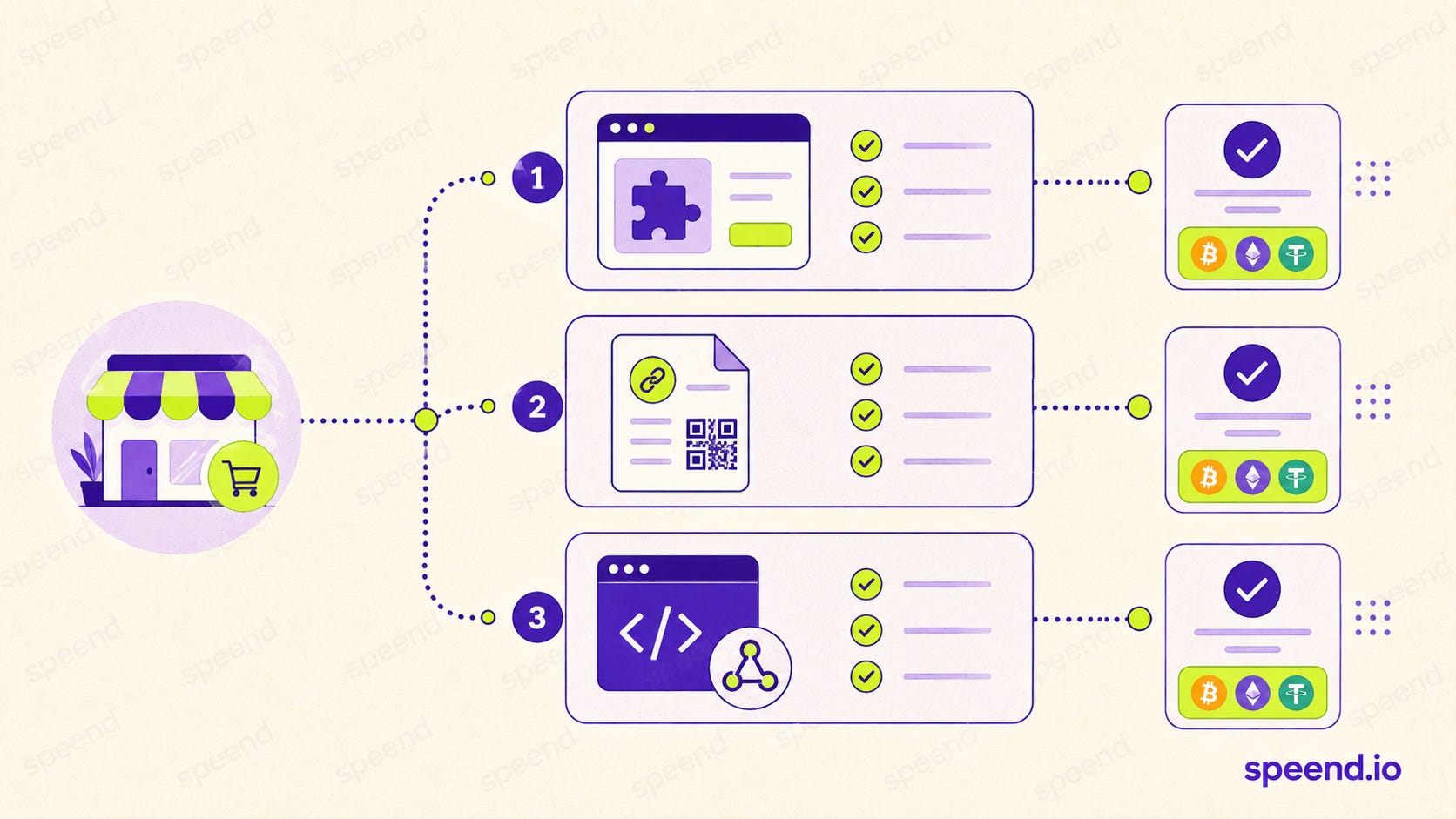

How to accept crypto payments on website: three integration paths

There are three working ways to add a crypto checkout to a site, and most merchants end up using two of them.

Path 1: Plugin or extension. The fastest route. If you run Shopify, WooCommerce, Magento, PrestaShop, OpenCart, or WHMCS, install the gateway’s plugin, paste in your API keys, and map your invoice statuses. Most teams have a working sandbox checkout the same day.

Path 2: Hosted invoice or payment link. No code required. Generate a link from your gateway dashboard, then paste it into an email, a contract, an invoice, or a WhatsApp message; the customer pays through a hosted page; the gateway notifies you. Useful for B2B invoicing, freelancers, and any business that doesn’t run a CMS at all.

Path 3: REST API. The deepest route. Use it when you need a fully native checkout, custom invoice logic, marketplace splits, or programmatic mass payouts. Speend’s API exposes invoice creation, webhook callbacks, conversion controls, and bulk payout endpoints; a small team can ship a working integration in a single sprint.

Most production setups combine paths 1 and 3: e-commerce front end on a plugin, back-office payouts on the API.

Compliance, KYC/KYB, and regional rules

Crypto payments are legal in most jurisdictions where you’d realistically operate, but the rules are not uniform. The EU’s Markets in Crypto-Assets Regulation (MiCA) sets the bar in Europe; the UK requires FCA registration for crypto-asset firms; the US enforces mostly through state Money Transmitter Licenses and federal AML rules under FinCEN. On the merchant side, you generally don’t need a crypto license to accept crypto. The gateway carries that compliance load, which is one of the structural reasons gateways exist.

Two practical points worth flagging. KYB (Know Your Business) is now standard at every reputable processor; budget 24 hours to a few days. And tax reporting: in most jurisdictions, crypto received as revenue is taxable at the fiat-equivalent value at the moment of receipt, which is what your gateway’s CSV exports are for. The IRS treats digital assets as property; HMRC treats receipts as ordinary income; the structure is broadly similar across G20 economies.

How long does crypto payment integration take?

Plugin installs take hours. Hosted payment links take minutes. Custom REST API integrations take a few days of engineering, or a week or two if you include finance reconciliation testing. The 2-to-4-week estimate vendor pages quote is a worst case; it assumes a custom build with full sandbox-to-production hardening. For most merchants, the bottleneck is KYB clearance, not the code.

What about volatility?

Volatility is a real risk only if you choose to hold the asset received. Auto-converting to USDT, USDC, EUR, or USD at the moment of payment carries no volatility exposure; the gateway absorbs the conversion. Most merchants pick a hybrid policy: convert customer-facing receipts to a stablecoin or fiat, keep a treasury allocation in BTC or ETH if the business has the appetite for it.

What fees should you expect?

A working frame for 2026:

Headline gateway fees of 0.4% to 1.5% per transaction, scaling down with volume.

Network fees that vary per chain. USDT-TRC20 is cheap; ETH mainnet runs expensive in busy periods; Solana and Polygon sit in the middle.

Conversion spreads of 0.1% to 0.5% on top of the published rate.

Withdrawal fees, either flat or as a percentage, when you off-ramp to a bank.

Compare this against card processing (1.5% to 3.5% plus a flat per-transaction fee, plus chargeback exposure that adds another 0.5% to 2% on contested verticals) and the math is rarely close. Even after every layer is counted, accepting crypto comes out as the cheaper rail in nearly every comparison.

Are crypto payments safe for merchants?

Yes, when handled through a regulated gateway. Blockchain transactions are cryptographically verified and immutable, which removes fraud vectors that plague card payments. The two real risks are operational, not technical: holding volatile assets without a hedge, and weak internal access controls on the merchant dashboard. Both are solved by configuration, not by avoiding the rail.

A final note on choosing first

Most merchants overthink the gateway decision and underthink the integration discipline that follows. The gateway can be swapped; the bookkeeping practices you build around it cannot. Pick a provider that gives you a working sandbox in a day, lets you go live in minutes once KYB clears, and answers the phone when something breaks. Speend is built around exactly that operational shape: 300+ coins, fast onboarding, friendly API, mass payouts and crypto payrolls, a personal manager who actually picks up.

Crypto acceptance in 2026 is a commercial decision that pays for itself in fees saved, chargebacks avoided, and customers reached. The question isn’t whether to add it. It’s which provider you pick before your competitors do.

Get started at speend.io.