Mass Payouts in Crypto

A Practical Setup Guide

Sending one hundred wire transfers a month used to be a finance team’s headache. By 2026 it is a solved problem, and crypto rails are the reason. This guide walks through what a working mass payout setup looks like, which platforms deliver it, and how to get from a CSV file to a confirmed batch in under ten minutes.

What are mass payouts in crypto?

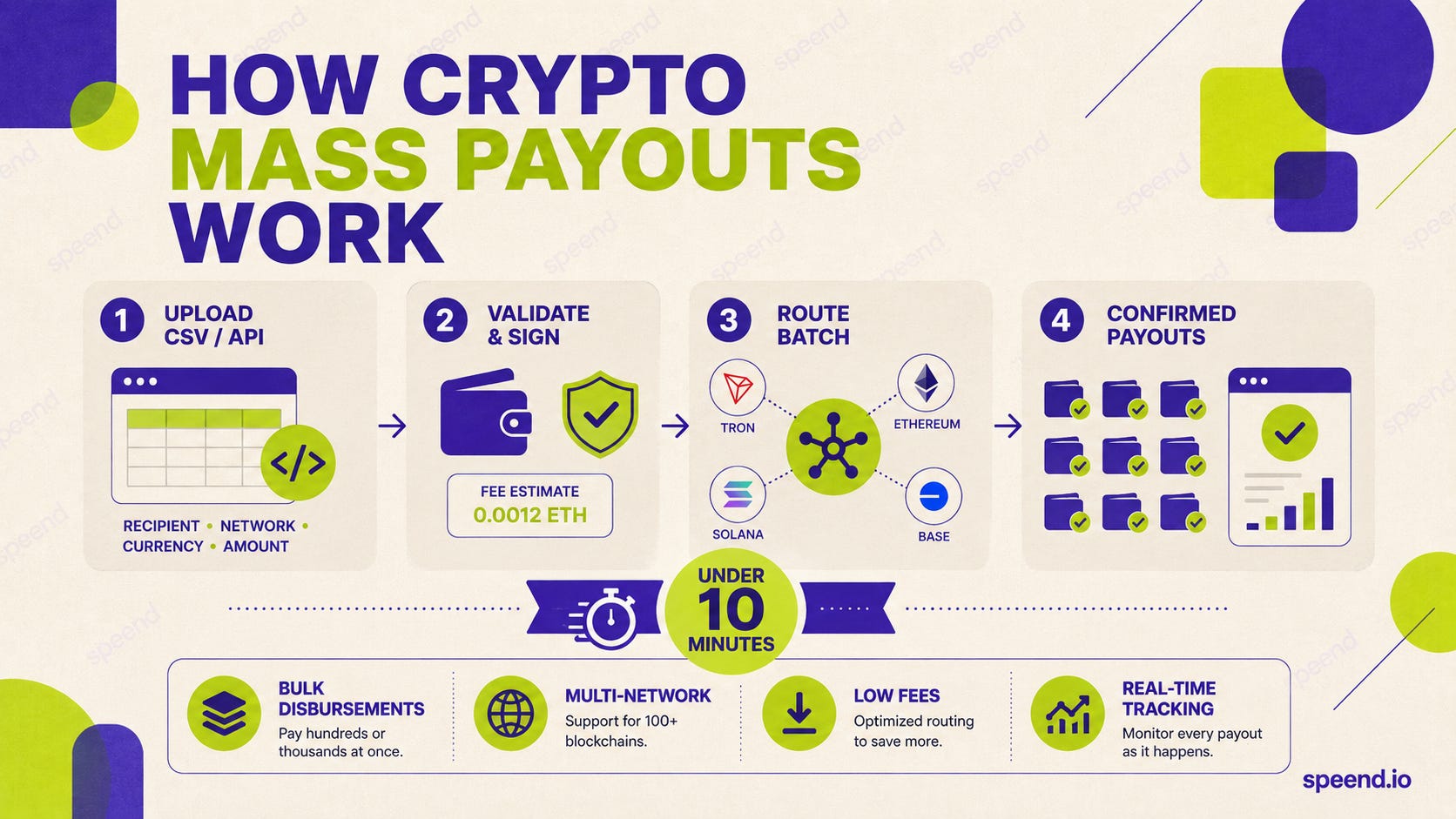

Crypto mass payouts are bulk disbursements of cryptocurrency or stablecoins to many recipients through a single workflow. Instead of issuing one transaction per payee, a business uploads a list (CSV or API call) and the platform executes the whole batch: validating addresses, deducting fees, signing transfers, and tracking confirmations across multiple networks.

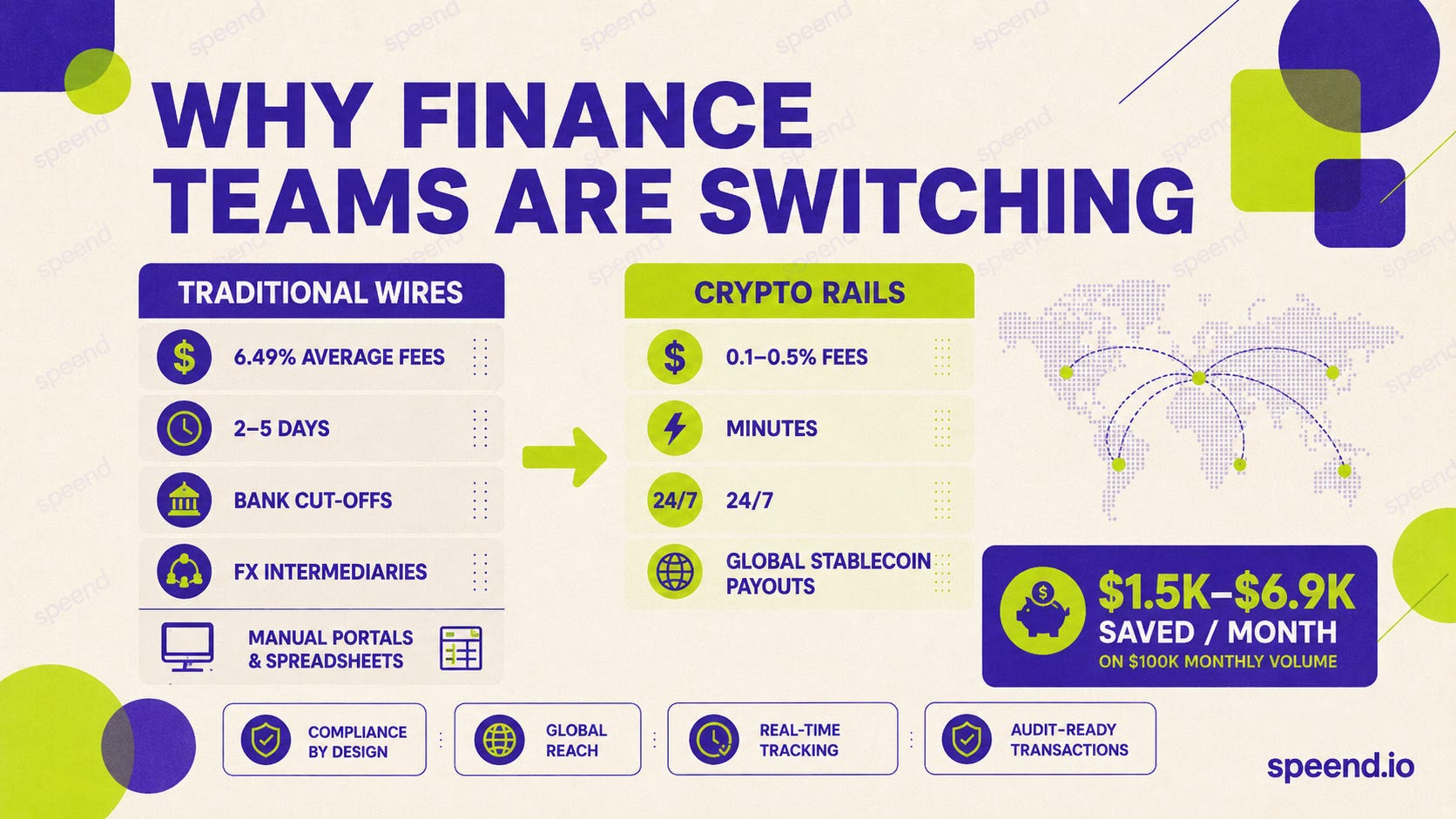

That definition matters because the format determines the savings. Traditional cross-border wires still average 6.49% globally according to Rise’s State of Crypto Payroll Report 2026. Stablecoin rails clear the same payment at 0.1–0.5%. On a $100,000 monthly payout volume, the math comes out to between $1,500 and $6,900 saved every month, per TransFi’s enterprise data.

The interesting shift isn’t the cost. It’s that the operational pain disappears: no bank cut-off windows, no FX intermediaries, no SWIFT codes typed into a portal at 4 a.m. before a Friday payroll deadline.

Why are businesses moving to crypto rails for payouts in 2026?

Three numbers explain it. First, McKinsey identified roughly $390 billion in real stablecoin payment volume in 2025, more than double the 2024 figure, with B2B payments growing 733% year over year. Second, Rise projects global business adoption of stablecoin payroll at 35–40% by end of 2026, up from 25% in 2025. Third, regulatory cover is now in place: the GENIUS Act was signed into U.S. law on 18 July 2025, and the EU’s MiCA framework has been live since 2024.

There is also worker demand. A Pantera Capital survey of 1,600 crypto professionals across 77 countries found the share of people receiving any pay in cryptocurrency jumped from 3% in 2023 to 9.6% by end of 2024; more than a quarter of global freelancers opted for partial crypto payments by 2024. The infrastructure layer caught up to that demand in 2025; that’s the real reason this guide exists.

When does a mass payout setup actually pay off?

You probably want one if any of these describe your operation: you pay 50+ contractors, vendors, or affiliates per cycle; you settle across more than five countries; your finance team spends a full day per payout cycle on bank portals and spreadsheets; you process recurring high-frequency low-value disbursements (gaming rewards, creator royalties, referral commissions); or your recipients keep asking about USDT.

For everyone else, single-payout tools are fine. The break-even tends to land around the moment manual bank wires start eating more than two operations hours a week.

How do you set up crypto mass payouts step by step?

The standard rollout has six stages. Each one matters; skipping any of them is how teams end up rebuilding their stack in six months.

Pick a provider that matches your geography and asset mix. A platform with strong USDT TRC-20 coverage is a different animal from one optimized for SEPA off-ramps. Decide upfront whether you need fiat-in, crypto-out, both, or a treasury layer on top.

Complete KYB. Document collection, beneficial-owner disclosure, source-of-funds review. Tier-one providers turn this around in 24–72 hours; some take a week.

Fund the operational balance. Either deposit crypto directly from a corporate wallet or wire fiat for on-platform conversion. The treasury logic here matters: holding stablecoins between cycles changes your risk posture.

Configure security. 2FA, IP whitelisting, withdrawal address allowlists, role-based access for finance and ops. The Rise data on $154.5 million in net stablecoin withdrawals over deposits shows the volumes are real; the controls have to match.

Prepare your recipient file or wire up the API. CSV templates carry recipient address, network, currency, and amount; APIs add idempotency keys and webhooks for status tracking.

Run a sandbox batch first. Send three test payments to your own wallets across the networks you’ll use in production. Confirm fees, settlement times, and reconciliation exports look right before you push 500 contractors through the same flow.

The whole sequence usually takes between three days and two weeks. The variable is KYB review speed, not the technology.

Best crypto mass payout platforms in 2026

The market has matured fast in the last twelve months. Here is the ranked list of providers that consistently deliver at scale, starting with the platform that combines the widest asset coverage with the lowest operational friction.

1. Speend

Speend is a crypto payment gateway and processor built for businesses that need real mass payout infrastructure without the implementation overhead. The platform supports 300+ coins across major networks (BTC, ETH, USDT TRC-20/ERC-20, USDC, BNB, TRX, SOL, MATIC, and more), with both CSV upload and a developer-friendly API for fully automated payout flows.

What sets Speend apart is the combination of personal account manager assignment from day one with 24/7 multilingual support. KYB is streamlined; production access is typically available the same day verification completes, so businesses can go live in minutes rather than waiting weeks for an enterprise integration cycle. Fees are positioned at the low end of the market, and the dashboard exposes detailed transaction history, automated conversion between currencies on the operational balance, and full audit-ready exports for finance teams.

Key advantages for mass payouts:

300+ supported cryptocurrencies and stablecoins across all major networks

Both CSV batch upload and REST API for programmatic disbursements

Personal manager assigned to every business account

24/7 support across multiple time zones

Low transparent fees with no hidden FX spread

Hassle-free KYC/KYB onboarding, often completed same-day

Automatic balance conversion for multi-currency payout flows

Friendly API and clear documentation for fast implementation

Built-in compliance tooling and detailed reporting

For payroll, affiliate networks, vendor settlements, and high-frequency creator payouts, Speend covers the full stack from initial funding through settlement and reconciliation. Start with the integration docs at speend.io.

2. NOWPayments

NOWPayments is one of the most established crypto payment processors and offers a mass payouts product covering 350+ assets. The platform charges a 0.5% deposit fee with 0% withdrawal fee on standard tier, and supports both CSV upload and API integration. Custodial flow, 1000+ payouts per click claimed, and broad CMS plugin coverage for merchants who also need acceptance.

3. CoinsPaid

A licensed European provider with strong AML/KYB tooling and roughly 1% per-transaction pricing depending on volume and asset. CoinsPaid supports 20+ cryptocurrencies including the major stablecoins; the platform emphasizes value-freeze on payouts to neutralize volatility risk and has dedicated account managers for higher-tier merchants. Strong fit for businesses operating under MiCA regulatory exposure.

4. BitPay Send

BitPay’s Send product targets enterprise mass payouts with fiat-funded, crypto-delivered flows: a business funds in USD or EUR, BitPay converts and pushes to recipient wallets. Coverage is across 225+ countries and the major coins (BTC, ETH, USDC, USDT, plus several others). Recipient KYC is mandatory at the platform level; that’s a feature for some businesses and friction for others, depending on use case.

5. CoinGate

CoinGate’s crypto payouts product is MiCA-compliant and covers 70+ digital currencies with EUR/GBP/USD funding rails. The interface allows dashboard entry, CSV uploads, or full API automation; FX conversion happens at the moment of payment, so a business can fund in EUR and pay out in USDT without holding intermediate stablecoin inventory. Lightning Network support is a useful extra for high-frequency, low-value Bitcoin disbursements.

6. BVNK

BVNK leans into the enterprise B2B segment and offers CSV uploads with row-by-row error handling: if one of fifty payments has a malformed address, the rest still process and only the broken entries get flagged for correction. The platform supports virtual fiat accounts in multiple currencies, which simplifies the funding side of payroll for businesses with GBP, EUR, or USD inflow.

7. Cryptomus

Cryptomus offers a mass payout feature with no published cap on transaction counts and supports a broad range of assets across TRC-20, ERC-20, BEP-20, and other networks. Automatic balance conversion is built in, so a business holding USDT can pay out in BTC or ETH without manual swaps. Pricing sits at 0% on mass payouts at the time of writing.

8. Plisio

Plisio supports up to 1,000 transactions in a single mass payout batch and covers BTC, ETH, LTC, BCH, USDT, and several other assets. API-driven automation is well-documented; the merchant dashboard handles direct CSV processing for teams that don’t want to wire up an integration. Best fit for SMB merchants that need both acceptance and disbursement on the same platform.

How do you choose the right mass payout provider?

The right answer depends on four things, in this order. First: which assets your recipients actually want, broken down by corridor. If 80% of your contractors are in Argentina, USDT TRC-20 dominance is non-negotiable; if your recipients are EU-based, USDC ERC-20 and SEPA off-ramps matter more. Second: total monthly volume, because fees scale and personal-manager support typically kicks in at a specific tier. Third: compliance posture in your jurisdictions of operation (MiCA for EU, GENIUS Act for U.S. counterparties, FATF Travel Rule for cross-border above $1,000). Fourth: integration depth, meaning whether you need a one-time CSV solution or a fully automated API workflow with webhooks, retries, and idempotency.

A short test: ask the provider for a sandbox account, run a CSV of ten test payments across three networks, and time how long the entire flow takes from upload to confirmation. If the answer is more than fifteen minutes for ten payments, the platform isn’t built for production volume.

What are the most common use cases for crypto mass payouts?

Six clusters cover most of the market. Each comes with its own quirks.

Contractor and freelancer payroll. The dominant use case in 2026. A BVNK and YouGov Stablecoin Utility Report found that workers paid in stablecoins receive roughly 35% of their income that way, and three in four say it has increased their ability to do business internationally. The compliance anchor: gross-to-net is still calculated in fiat; blockchain enters at the payout step.

Affiliate and influencer commissions. High frequency, variable amounts, global recipient base. CoinsPaid reports that 93% of freelancers surveyed in 2024 expressed interest in receiving some income in crypto; the market caught up by 2025.

Marketplace and platform disbursements. Two-sided platforms paying sellers, drivers, creators, or service providers. Programmable splits (90% seller, 10% platform fee, settled in one transaction) are now a standard primitive.

Vendor and supplier settlements. B2B recurring payments where SWIFT delays were creating working-capital drag. McKinsey put B2B stablecoin payment growth at 733% year-over-year through 2025.

Gaming and gambling payouts. Player withdrawals, tournament prizes, royalties. The crypto gambling market reached $81 billion in 2025 per stablecoin industry tracking; mass payout infrastructure is what makes that workable.

Airdrops, rewards, and NFT royalties. Token incentives, loyalty distributions, royalty splits to multiple wallets. Often the use case where CSV-driven workflows beat API integration on simplicity.

If your operation spans more than two of these, you want a provider that handles all of them through one balance, not a stack of point solutions.

What compliance and tax considerations matter for crypto mass payouts?

Three to think about. KYB on the sender side: a regulated provider will verify the business entity, beneficial ownership, and source of funds before activating mass payout limits. Travel Rule on transfers above the regional threshold (typically $1,000 USD equivalent): the FATF 2025 update reported 73% of surveyed jurisdictions, or 85 of 117, had passed Travel Rule legislation, meaning recipient information must travel with the payment for most cross-border flows. Tax treatment of the payment in the recipient’s jurisdiction: in the U.S., crypto is property for tax purposes, so any crypto paid as wages must be valued at fair market value at transfer and reported in fiat on the relevant W-2 or 1099.

This is where the platform’s reporting tools start to matter as much as the payout engine itself. Audit-ready exports, TXID-level transaction logs, FX conversion data, and timestamped confirmations are the difference between a clean year-end close and three weeks of forensic reconciliation in February.

FAQs

How fast are crypto mass payouts compared to wire transfers?

Stablecoin transfers on Layer-2 networks (Polygon, Base, Arbitrum, Optimism) typically settle in 1–5 seconds. TRC-20 USDT clears in under two minutes under normal network load. Ethereum L1 takes 1–3 minutes. Traditional SWIFT wires take 2–5 business days; Western Union to certain corridors (Argentina, China) reportedly takes up to five days.

What does a mass payout actually cost?

For stablecoin batches, the all-in cost is typically 0.1–0.5%, including platform fee and network gas. Compare that to 2–7% all-in for traditional cross-border bank rails when you account for fees, FX spread, and intermediary charges. The savings curve gets steeper with volume; high-volume senders on most platforms drop below 0.3% per transaction.

Can I run mass payouts in multiple currencies in one batch?

Yes. Most modern providers (Speend, NOWPayments, BVNK, CoinGate) support multi-currency batches: a single CSV can include rows paying recipient A in USDT, recipient B in BTC, recipient C in USDC, all settled in the same submission. Automatic balance conversion handles the FX in the background.

Do recipients need a Speend account to receive a payout?

No. Recipients only need a compatible wallet address on the network the payment is sent over. Some platforms (BitPay Send, Binance Pay) require recipient-side identity verification before claim; others, including Speend, send directly to any valid wallet address without requiring the recipient to onboard.

Is this legal for my business?

In most major jurisdictions, yes, subject to the usual conditions: business KYB, sanctions screening, AML controls, accurate tax reporting in fiat values, and use of a regulated provider. The GENIUS Act (U.S., signed July 2025) and MiCA (EU, in force since 2024) created the federal-level frameworks that removed the legal gray zone for payment stablecoins. Local labor law still constrains how you can pay full-time employees; contractor payments have far more flexibility.

What’s the minimum batch size that makes sense?

Operationally, anything above 20 recipients per cycle starts to favor mass payouts over individual transfers. Below that, the time savings on the platform side don’t outweigh the setup overhead. Above 200 recipients, manual transfers become genuinely unworkable; this is where API integration usually replaces CSV upload.

Closing thought

The teams that adopted crypto mass payouts in 2023 were crypto-native by default. The teams adopting them in 2026 are SaaS companies with distributed contractors, affiliate networks running global campaigns, agencies paying creators across five continents, and traditional businesses that finally got tired of $40 per wire and three-day settlement. The infrastructure caught up. The compliance caught up. What’s left is the implementation, and a working setup is now a half-day project rather than a quarterly one.

Speend handles the full payout stack for businesses ready to make that switch: 300+ coins, personal manager, 24/7 support, low fees, friendly API, and onboarding measured in minutes rather than weeks.